Unit 6: The BlueCard® Program

2.6 What is the BlueCard Program?

2.6 How the Program Works: An Example

2.6 How to Identify BlueCard Members

2.6 Medicaid Programs Administered by BluePlans

2.6 Consumer Directed Healthcare and Health Care Debit Cards

2.6 Health Insurance Marketplaces

2.6 Blue Exchange for Inquiries and Authorizations

2.6 BlueCard Eligibility and Benefits Verification

2.6 Electronic Provider Access (EPA)

2.6 Claim Submission and Claim Status Inquiry

2.6 Itemized Bills Required for High-Dollar Host Claims

2.6 New Audit Requirements for Million-Dollar Claims

2.6 Contiguous County and Eligible Affiliate Contracting

2.6 Ancillary Claim Filing Rules

2.6 Medicare Advantage Products

2.6 Medicare Advantage PPO Network Sharing (DE, PA, and WV Only)

2.6 Medicare Advantage Eligibility, Claims and Payment

The 35 independent, community-based and locally operated Blue Cross and Blue Shield companies and the Blue Cross and Blue Shield Association (BCBSA) comprise the Blue Cross and Blue Shield System, the nation's oldest and largest family of health benefits companies. The Blues cover 100 million Americans in all 50 states, the District of Columbia, and Puerto Rico. Nationwide, more than 96% of hospitals and 91% of professional providers contract with the Blue System — more than any other health insurer.

Offering a variety of products, programs, and services to all segments of the population, the Blues cover large employer groups, small business, and individuals. Moreover, the Blues have enrolled more than half of all U.S. federal workers, retirees, and their families, making the Federal Employee Program (FEP) the largest single health plan group in the world.

As a participating provider of Highmark, you may render services to patients who are members of other Blue Plans traveling to or living in Pennsylvania, Delaware, and West Virginia.

This unit describes the BlueCard Program and its advantages, and provides information to make filing claims easy. You will find helpful information about:

- Identifying members

- Verifying eligibility

- Obtaining precertifications/preauthorizations

- Filing claims

- Who to contact with questions

BlueCard® is a national program that enables members of one Blue Plan to obtain health care service benefits while traveling or living in another Blue Plan’s service area. The program links participating health care providers with the independent Blue Cross Blue Shield (BCBS) Plans across the country and in more than 200 countries and territories worldwide through a single electronic network for claims processing and reimbursement.

The program lets you submit claims for patients from other Blue Plans, domestic and international, to your local Blue Plan. Highmark is your sole contact for claim submission, payment, adjustments, and issue resolution.

The BlueCard Program lets you conveniently submit claims for members from other Blue Plans, including international Blue Plans, directly to Highmark. Highmark will be your one point of contact for all of your claims-related questions.

Always look to Highmark first when you need help with information about out-of- area members. We are committed to meeting your needs and expectations. In doing so, your out-of-area Blue Plan patients will have a positive experience with each visit.

Highmark Networks Supporting BlueCard

The BlueCard Program is supported by Highmark’s networks as follows:

Delaware

The Delaware Provider Network supports the BlueCard Program.

New York

- Northeastern New York: Northeastern New York Provider Networks support the BlueCard Program.

- Western New York: Western New York Provider Networks support the BlueCard Program.

Pennsylvania

Participating Provider Network: Supports all BlueCard programs for members with traditional, POS, or HMO coverage who are traveling or living outside of their Blue Plan’s service area.

Keystone Health Plan West (KHPW)*: The KHPW network supports the BlueCard PPO programs in the 29-county Western Region of Pennsylvania for members in a PPO plan who are traveling or living outside of their Blue Plan’s service area.

Premier Blue Shield Network: The Premier Blue Shield Network supports the BlueCard PPO programs in all other Highmark service areas in Pennsylvania for members in a PPO plan who are traveling or living outside of their Blue Plan’s service area.

*Keystone Health Plan West is Highmark’s managed care provider network in the 29-county Western Region of Pennsylvania.

West Virginia

- Indemnity Network: Supports the BlueCard programs for members with traditional or HMO coverage who are traveling or living outside of their Blue Plan’s area.

- Preferred Provider Organization (PPO) Network: Supports the BlueCard PPO programs for members in a PPO plan who are traveling or living outside of their Blue Plan’s service area.

- Point of Service (POS) Network: Supports the BlueCard POS programs for members in a POS plan who are traveling or living outside of their Blue Plan’s service area.

BlueCard Program Exclusions

Claims for the following products are excluded from the BlueCard Program:

- Stand-alone dental

- Self-administered prescription drugs delivered through an intermediary model (using a vendor)

- Vision delivered through an intermediary model (using a vendor)

- The Federal Employee Program (FEP)*

- Medicare Advantage**

- Medicaid and State Children’s Health Insurance Program (SCHIP) products that are part of state’s Medicaid program

*For more information on FEP, please visit the manual’s Chapter 2.3: Other Government Programs and for billing tips, see Chapter 6.4: Professional (1500/837P) Reporting Tips.

**Medicare Advantage is a separate program from BlueCard and delivered through its own centrally administered platform; however, since you may see members of other Blue Plans who have Medicare Advantage coverage, Medicare Advantage information is available in this unit.

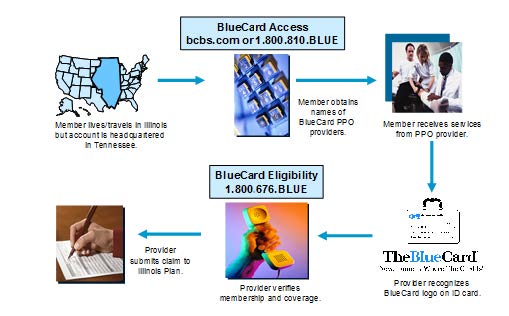

The following diagram illustrates how the BlueCard® program works. In this example, a member with coverage through BlueCross BlueShield of Tennessee is seeking services in Illinois.

There are two scenarios where a Tennessee member might need to see a provider in the Illinois Blue Plan’s service area:

- If the Tennessee member was traveling in Illinois; or

- If the member resides in Illinois and has employer-provided coverage through BlueCross BlueShield of Tennessee.

How the Member Can Find Participating Providers

In either scenario above, the member can obtain the names and contact information for BlueCard PPO providers in Illinois by calling the BlueCard Access Line at 800-810-BLUE (2583).

The member also can obtain information online by using the BlueCard National Doctor and Hospital Finder available at bcbs.com.

Note: Although members are not obligated to identify participating providers through either of these methods, it is their responsibility to go to a PPO provider if they want to access PPO in-network benefits.

How a Provider Verifies the Member's Eligibility and Benefits

When the member makes an appointment and/or sees an Illinois BlueCard PPO provider, the provider may verify the member’s eligibility and coverage information via the BlueCard Eligibility Line at 800-676-BLUE (2583).

The provider may also obtain this information via a HIPAA electronic eligibility transaction if the provider has established electronic connections for such transactions with the local Plan, Blue Cross and Blue Shield of Illinois

Claim Submission and Payment

After rendering services, the provider in Illinois files a claim locally with Blue Cross and Blue Shield of Illinois. The Illinois Blue Plan forwards the claim internally to BlueCross BlueShield of Tennessee.

The Tennessee Blue Plan adjudicates the claim according to the member’s benefits and the provider’s arrangement with the Illinois Plan. This information is sent back to Blue Cross and Blue Shield of Illinois.

When the claim is finalized, the Tennessee Plan issues an explanation of benefit (EOB) to its member. The Illinois Plan issues the explanation of payment or remittance advice to its provider and pays the provider.

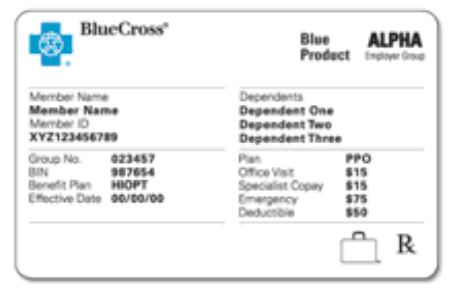

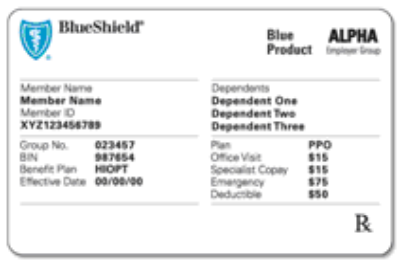

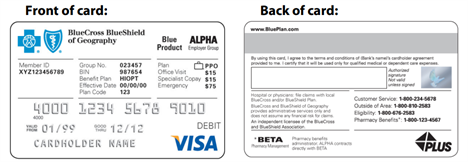

When members of out-of-area Blue Plans arrive at your office, be sure to ask them for their current Blue Plan membership identification card. The card will display the member’s identification number.

Important facts concerning Member IDs:

- The main identifier for out-of-area members is the prefix.

- A correct Member ID number includes the prefix (first three positions) and all subsequent characters, up to 17 positions total. This means that you may see cards with ID numbers between 6 and 14 numerals/letters following the prefix.

- Do not add/delete characters or numerals within the Member ID.

- Do not make up prefixes.

- Do not change the sequence of the characters following the prefix.

- The prefix is critical for the electronic routing of specific HIPAA transactions to the appropriate Blue Plan.

Do not assume that the member’s ID number is the social security number. All Blue Plans have replaced social security numbers on Member ID cards with an alternate, unique identifier.

Note: Members who are part of the Blue Cross Blue Shield Federal Employee Program (FEP), which is excluded from BlueCard, will have the letter "R" in front of their Member ID number instead of a 3-character prefix.

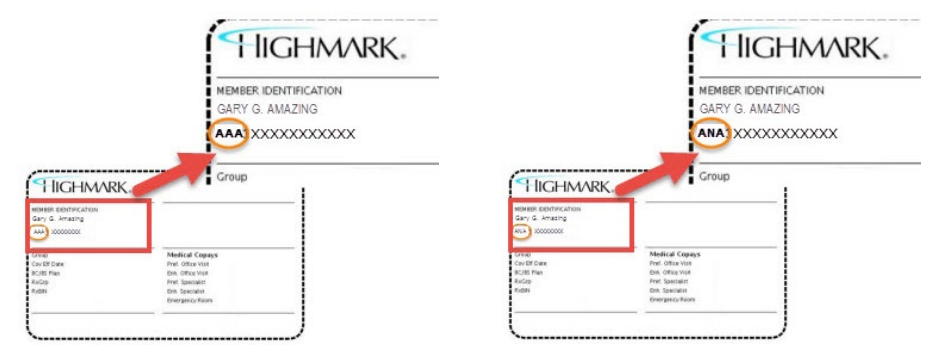

Prefix (Formerly "Alpha Prefix")

The 3-character prefix at the beginning of the member’s identification number is the key element used to identify and correctly route claims. The prefix identifies the Blue Plan or national account to which the member belongs. It is critical for confirming a patient’s membership and coverage.

The 3-character prefix has historically been an “alpha prefix” – with all alpha characters. Beginning in 2018, the Blue Cross Blue Shield Association (BCBSA) issued alphanumeric “prefixes” to Blue Plans since the options for 3-character all alpha combinations were running low. The examples below illustrate the alpha and alphanumeric prefixes on the Member ID card (A = alpha; N = numeric):

There will be no change to existing 3-character alpha prefixes for products/accounts already in existence. Alphanumeric prefixes will be created and assigned to Blue Plans for new products or new large national group accounts.

Examples of Member ID Numbers

The following examples represent various numeral/letter combinations that may be seen as Member IDs for Blue Plan members (A = alpha; N = numeric):

Remember: Member ID numbers must be reported exactly as shown on the ID card and must not be changed or altered. Do not add or omit any characters from the Member ID.

As a provider servicing out-of-area members, you may find the following tips helpful:

- Ask the member for the most current ID card at every visit. Since new ID cards may be issued to members throughout the year, this will ensure that you have the most up-to-date information in your patient’s file.

- Verify with the member that the ID number on the card is not his/her Social Security Number. If it is, call the BlueCard Eligibility Line at 800-676-BLUE to verify the ID number.

- Make copies of the front and back of the member’s ID card and pass this key information on to your billing staff.

- Capture all ID card data to ensure accurate claim processing. If the information is not captured correctly, you may experience a delay with the claim processing.

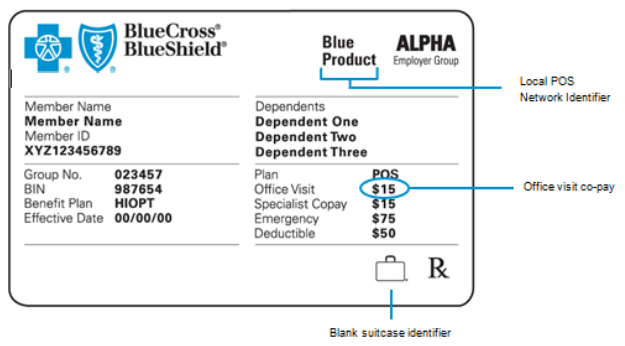

Suitcase Logos

BlueCard Member ID cards have a suitcase logo, either as an empty suitcase or as a PPO in a suitcase.

The PPO in a suitcase logo indicates that the member is enrolled in either a PPO product or an Exclusive Provider Organization (EPO) product. In either case, you will be reimbursed according to Highmark’s PPO provider contract.

Note: EPO products may have limited benefits out-of-area. The potential for such benefit limitations are indicated on the reverse side of an EPO ID card.

One of the key elements of health care reform under the Affordable Care Act (ACA) is the public "exchange" - officially known as the Health Insurance Marketplace. The PPOB in a suitcase logo on an ID card indicates that the member has a Blue Plan PPO or EPO product from the exchange. These members have access to a Blue System PPO network referred to as “BlueCard PPO Basic.”

Many Blue Plans have created a new BlueCard PPO Basic network; however, Highmark will utilize the same networks as we do for BlueCard PPO. You will be reimbursed for covered services in accordance with your PPO contract with Highmark.

The empty suitcase logo indicates that the member is enrolled in one of the following products: traditional, Health Maintenance Organization (HMO), or Point of Service (POS). For members with these products, you will be reimbursed according to Highmark’s traditional participating provider contract.

Blue Plan ID Cards Without Suitcase Logos

Some Blue Plan ID cards do not have a suitcase logo. Those are the ID cards for Medicaid; State Children’s Health Insurance Programs (SCHIP), if administered as part of a state’s Medicaid program; and Medicare complementary and supplemental products, also known as Medigap.

Government determined reimbursement levels apply to these products. While Highmark routes all of these claims for out-of-area members to the member’s Blue Plan, most of the Medicare complementary or Medigap claims are sent directly from the Medicare intermediary to the member’s Blue Plan via the established electronic Medicare crossover process.

BlueCard Managed Care/POS Program Members

The BlueCard Managed Care/POS Program is for members who reside outside their Blue Plan’s service area. Unlike in the BlueCard PPO Program, the BlueCard Managed Care/POS members are enrolled in a Highmark network and have a primary care physician (PCP).

You can recognize BlueCard Managed Care/POS members who are enrolled in a Highmark network through the Member ID card as you do for all other BlueCard members. The ID cards will include:

- The 3-character prefix at the beginning of the member’s ID number

- A local network identifier

- The blank suitcase logo

Medicaid is a government program that provides free or low-cost health care to an eligible population. States design their own Medicaid programs within federal guidelines – eligible populations, cost-sharing, benefits, and other rules vary by state. State Medicaid agencies contract with health insurers, including Blue Cross and Blue Shield (BCBS) Plans, as Managed Care Organizations (MCOs) to administer comprehensive Medicaid benefits.

Medicaid members have limited out-of-state benefits, generally covering only emergent situations. In some cases, such as continuity of care, children attending college out of state, or a lack of specialists in the member’s home state, a Medicaid member may receive care in another state, and generally the care requires authorization. Reimbursement for covered services is limited to the Medicaid allowed amount established in the member’s home state.

Blue Plan Medicaid ID Cards

Members enrolled in BCBS Medicaid plans are issued ID cards from the home plan where they reside, and are usually provided with state-issued Medicaid ID cards. It is important to note that:

- Blue Plan Medicaid ID cards do not always indicate that a member has a Medicaid product.

- Blue Plan Medicaid ID cards do not have the suitcase logo.

- The back of the Blue Plan Medicaid ID card must contain a disclaimer indicating limited out-of-area benefits.

Providers should submit an eligibility inquiry if the ID card has no suitcase logo and has a disclaimer with benefit limitations.

Obtaining Eligibility and Benefits and Prior Authorization

You can obtain eligibility and benefit information for out-of-area BCBS Medicaid members using the same tools as you would for other out-of-area Blue Plan members:

- Submit an eligibility inquiry using Availity;

- Submit a HIPAA 270/271 electronic eligibility inquiry; or

- Call the BlueCard Eligibility line at 800-676-BLUE (2583).

Providers can also request prior authorization for out-of-area Blue Plan Medicaid members using the same tools available for BlueCard:

- BlueExchange;

- BlueCard Eligibility Line at 800-676-BLUE (2583); and

- Electronic Provider Access (EPA) tool for pre-service review, including prior authorization.

Claim Submission and Reimbursment

Although BCBS Medicaid claims are processed through the BCBS Inter-Plan system, Medicaid is not officially part of the BlueCard Program since there is no network reciprocity and the locally negotiated rates do not apply to Medicaid claims. However, you still submit out-of-area Blue Plan Medicaid claims to Highmark as you would submit BlueCard claims, and you will receive reimbursement from Highmark. You will be reimbursed according to the member’s home state Medicaid fee schedule, which may or may not be equal to what you are accustomed to receiving for the same service in your state.

When you see a Blue Plan Medicaid member from another state, you must accept the Medicaid allowed amount applied in the member’s home state even if you do not participate in Medicaid in your own state. Federal regulations limit providers to the Medicaid allowed amount applicable in the member’s home state as payment in full. Billing Medicaid members for the amount between the Medicaid allowed amount and charges for Medicaid-covered services is specifically prohibited by Federal regulations(42 CFR 447.15).

In some circumstances, a state Medicaid program will have an applicable copay, deductible, or coinsurance applied to the member’s plan. You may collect this amount from the member as applicable. Note that the coinsurance amount is based on the Medicaid fee schedule in the member’s home state for that service.

If you provide Medicaid services to a member who is not covered by Medicaid, you will not be reimbursed. In some states, you may bill a Medicaid member for services not covered by Medicaid if you have obtained written approval from the member in advance of services being rendered.

Medicaid Provider Enrollment Requirements

Some states require that out-of-state providers enroll in their state’s Medicaid program in order to be reimbursed. Some of these states may accept a provider’s Medicaid enrollment in the state where they practice to fulfill this requirement. To view provider enrollment requirements for BCBS Medicaid states, please see the Medicaid Provider Enrollment Requirements by State. (This document is also available in the BlueCard Information Center on the Provider Resource Center; select Inter-Plan Programs from the main menu.)

If you are required to enroll in another state’s Medicaid program, you should receive notification upon submitting an eligibility or benefit inquiry. You should enroll in the state’s Medicaid program before submitting the claim. If you submit a claim without enrolling, your Medicaid claims will be denied and you will receive information from Highmark regarding the Medicaid provider enrollment requirements. You will be required to enroll before the Medicaid claim can be processed and before you may receive reimbursement.

Required Data Elements for Medicaid Claims

Medicaid MCOs are required to report specific Medicaid encounter information to their states and may incur a financial penalty if the data is not submitted or incomplete. State Medicaid encounter data reporting requirements vary from state to state. When billing for a Medicaid member, please remember to check the Medicaid website of the state where the member resides to understand the state’s Medicaid requirements for reporting encounter data elements.

The data elements identified below are required on all out-of-area Blue Plan Medicaid claims so that BCBS Medicaid MCOs are able to comply with encounter data reporting applicable to their respective state.

Effective March 2016, applicable Medicaid claims submitted without these data elements will be denied:

- National Drug Code (NDC)

- Rendering Provider Identifier (NPI)

- Billing Provider Identifier (NPI)

Applicable Medicaid claims submitted without these data elements may be pended or denied until the required information is received:

|

Billing Provider (Second) Address Line |

Ordering Provider Identifier and Identification Code Qualifier |

|

Billing Provider Middle Name or Initial |

Ordering Provider Identifier and Identification Code Qualifier |

|

(Billing) Provider Taxonomy Code |

Attending Provider NPI |

|

(Rendering) Provider Taxonomy Code |

Operating Physician NPI |

|

(Service) Laboratory or Facility Postal Zone or ZIP Code |

Claim or Line Note Text |

|

(Ambulance) Transport Distance |

Certification Condition Applies Indicator and Condition Indicator (Early and Periodic Screening, Diagnosis and Treatment [EPSDT]) |

|

(Service) Laboratory Facility Name |

Certification Condition Applies Indicator and Condition Indicator (Early and Periodic Screening, Diagnosis and Treatment [EPSDT]) |

|

(Service) Laboratory or Facility State or Province Code |

Service Facility Name and Location |

|

Value Code Amount |

Ambulance Transport Information |

|

Value Code |

Patient Weight |

|

Condition Code |

Ambulance Transport Reason Code |

|

Occurrence Codes and Date |

Round Trip Purpose Description |

|

Occurrence Span Codes and Dates |

Stretcher Purpose Description |

|

Referring Provider Identifier and Identification Code Qualifier |

Important: National Drug Codes (NDCs) are required on all applicable out-of-area Blue Plan Medicaid claims, including inpatient, outpatient, and professional; claims submitted without applicable NDCs reported will be denied.

Converting NDCS From 10-Digits to 11-Digits

Many NDCs are displayed on drug packaging in a 10-digit format. Proper billing of an NDC requires an 11-digit number in a 5-4-2 format. Converting NDCs from a 10- digit to an 11-digit format requires a strategically placed zero, dependent upon the 10-digit format.

The following table shows common 10-digit NDC formats indicated on packaging and the associated conversion to an 11-digit format, using the proper placement of a zero. The correctly formatted additional “0” is in a bold font and underlined in the following example. Note that hyphens indicated below are used solely to illustrate the various formatting examples for NDCs. Do not use hyphens when entering the actual data in your paper claim form.

Converting NDCs From 10-Digits to 11-Digits

|

10-Digit Format on Package |

10-Digit Format Example |

11-Digit Format |

11-Digit Format Example |

Actual 10-Digit NDC Example |

11-Digit Conversion of Example |

|

4-4-2 |

9999-9999-99 |

5-4-2 |

09999-9999-99 |

09999-9999-99 0002-7597-01 Zyprexa® 10mg Vial |

00002759701 |

|

5-3-2 |

99999-999-99 |

5-4-2 |

99999-0999-99 |

50242-040-62 Xolair® 150mg Vial |

50242004062 |

|

5-4-1 |

99999-9999-9 |

5-4-2 |

99999-9999-09 |

60575-4112-1 Synagis® 50mg Vial |

60575411201 |

The Blue Cross and Blue Shield Association licenses Blue Plans outside of the United States. International Licensees currently include the following:

- Blue Cross Blue Shield (BCBS) of U.S. Virgin Islands

- BlueCross and BlueShield of Uruguay

- Blue Cross and Blue Shield of Panama

- Blue Cross Blue Shield of Costa Rica

If in doubt, always check with Highmark as the list of International Licensees may change.

International Blue Plan ID Cards

The ID cards from International Licensees will also contain 3-character prefixes and may or may not have a benefit product logo. Please treat these members the same as domestic Blue Plan members (e.g., do not collect any payment from the member beyond cost-sharing amounts such as deductible, coinsurance, and copayment). Submit all claims for these international members to Highmark.

Canadian Association of Blue Cross Plans are Separate and Distinct

The Canadian Association of Blue Cross Plans and its member Plans are separate and distinct from the Blue Cross and Blue Shield Association (BCBSA) and its member Plans in the United States.

Claims for members of the Canadian Blue Cross Plans are not processed through the BlueCard Program. Please follow the instructions of these Canadian plans for servicing their members. Instructions may be provided on their ID cards.

The Blue Cross Plans in Canada are:

- Alberta Blue Cross

- Ontario Blue Cross

- Saskatchewan Blue Cross

- Manitoba Blue Cross

- Quebec Blue Cross

- Pacific Blue Cross

- Medavie Blue Cross

GeoBluesm health plans help travelers and expatriates get high quality, safe, and convenient care around the world and are offered in cooperation with many Blue Cross and Blue Shield companies, including Highmark. Through innovative product offerings, including concierge-level service and unsurpassed mobile technology, members who are living or working abroad can find carefully selected doctors and hospitals in more than 180 countries.

These plans provide medical coverage outside the United States for ongoing conditions, preventive health care, or an unexpected medical crisis. GeoBlue enables participating Blue Plans to provide their clients traveling the world with the care they need, when and where they need it, from trusted doctors and hospitals.

GeoBlue is the trade name for the international health insurance programs of Worldwide Insurance Services, an independent licensee of the Blue Cross Blue Shield Association.

Verifying Blue Plan patient's benefits and eligibility is now more important than ever since new products and benefit types have entered the market. In addition to patients who have traditional Blue PPO, HMO, POS, or other coverage with typically high lifetime coverage limits (i.e., $1 million or more), you may now see patients whose annual benefits are limited to $50,000 or less.

Currently, Highmark does not offer the limited benefit plans described here to our members; however, you may see patients with these limited benefit plans who are covered by another Blue Plan.

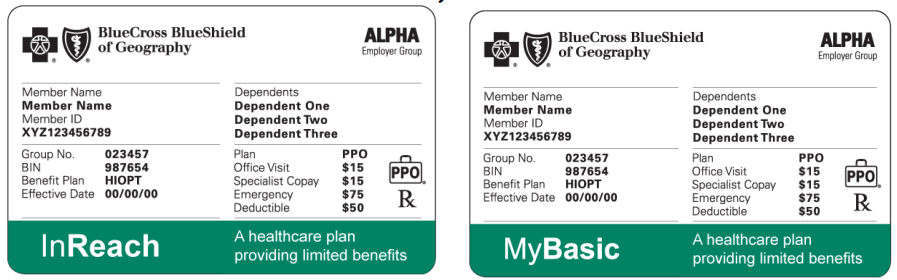

How to recognize members with limited benefits products Patients with Blue limited benefits coverage carry ID cards that may have one or more of the following indicators:

- Product name will be listed such as InReach or MyBasic;

- A green strip at the bottom of the card;

- A statement either on the front or back of the ID card stating that this is a limited benefit product;

- A black cross and/or shield to help differentiate it from other identification cards.

These Blue limited benefits ID cards may look like this:

Verify Eligibility and Benefits

In addition to obtaining a copy of the patient’s ID card, and regardless of the benefit product type, we recommend that you verify the patient’s eligibility and benefits. You may do so electronically or you may call the 800-676-BLUE Eligibility Line for out-of-area members.

Both electronically and via telephone, you will receive the patient’s accumulated benefits to help you understand the remaining benefits left for the member. If the cost of services extends beyond the patient’s benefit coverage limit, inform the patient of any additional liability they might have.

Annual benefit limits should be handled in the same manner as any other limits on the medical coverage. Any services beyond the covered amounts or the number of treatments are member liability.

We recommend you inform the patient of any potential liability they might have as soon as possible.

Some Blue Plans offer Reference Based Benefits to self-funded group accounts that limit certain (or specific) benefits to a dollar amount that incents members to actively shop for health care for those services.

The goal of Reference Based Benefits is to engage members in their health choices by giving them an incentive to shop for cost-effective providers and facilities. Reference Based Benefit designs hold the member responsible for any expenses above a calculated “Reference Cost” ceiling for a single episode of service.

Due to the possibility of increased member cost-sharing, Referenced Based Benefits will incent members to use Plan transparency tools, like the National Consumer Cost Tool (NCCT), to search for and identify services that can be performed at cost-effective providers and/or facilities that charge at or below the reference cost ceiling.

Reference Cost

The Blue Plan will pay up to a predetermined amount, called a “Reference Cost,” for specific procedures. If the allowed amount exceeds the reference cost, the excess amount becomes the member’s responsibility.

The Blue Cross Blue Shield Association (BCBSA) calculates reference costs on a state by state basis with each state representing a “cost region” with its own reference costs. The reference costs are established in a cost region based on claims data provided by the Blue Plan(s) in that region. Reference costs are updated on an annual basis.

Applicable Services

The Blue Plan and the employer group collaborate to define the services for which Referenced Based Benefits will apply. Services could include inpatient services, outpatient procedures, and diagnostic services; and services may vary by employer group with coverage under the same Blue Plan. Reference Based Benefits are not applicable to any service that is urgent or emergent.

Verifying Coverage

When you submit an electronic eligibility and benefits inquiry prior to performing services, you will be notified if a member is covered under Reference Based Benefits.

Additionally, you may call the BlueCard Eligibility phone number to verify if a member is covered under Referenced Based Benefits: 800-676-BLUE (800-676-2583).

Claims, Payment, and Member Responsibility

Reference Based Benefits do not alter the Highmark fee schedule. Providers are paid the applicable fee schedule allowance on all services where Reference Based Benefits apply.

When Reference Based Benefits are applied and the cost of the services rendered is less than the cost ceiling, then Highmark will pay eligible benefits as it has in the past. The member continues to pay their standard cost-sharing amounts in the forms of coinsurance, copay, or deductible as normal.

If the cost of the services rendered exceeds the reference cost ceiling, then Highmark will pay benefits up to that reference cost ceiling. The member continues to pay their standard cost-sharing amounts in the forms of coinsurance, copay, or deductible, as well as any amount above the reference cost ceiling up to the contractual amount.

Example 1: If a member has a reference cost of $500 for an MRI and the allowable amount is $700, then Highmark will pay up to the $500 for the procedure and the member is responsible for the $200.

Example 2: If a member has a reference cost ceiling of $600 for a CT scan and the allowable amount is $400, then Highmark will pay up to the $400 for the procedure.

Consumer Transparency Tools

Since members are subject to any charges above the Reference Cost up to the contractual amount for particular services, members may ask you to estimate how much a service will cost. Also, you can direct members to view their Blue Plan’s transparency tools to learn more about the cost established for an episode of care.

The National Consumer Cost Tool (NCCT) is a national effort by Blue Cross and/or Blue Shield Plans across the country to assist members in navigating the health care delivery system. A national database houses pre-calculated cost estimates submitted by Blue Plans, which allows members to view the total cost of specific medical procedures and common office visits for providers across the country.

Note: Highmark members have access to this information through the Care Cost Estimator which is available to them by logging into their account on Highmark’s websites.

Questions? If you have any questions regarding Reference Based Benefits, please contact the Highmark Provider Service Center.

Consumer Directed Healthcare (CDHC) is a broad term that refers to a movement in the health care industry to empower members, reduce employer costs, and change consumer health care purchasing behavior.

Health plans that offer CDHC provide the member with additional information to make an informed and appropriate health care decision through the use of member support tools, provider and network information, and financial incentives.

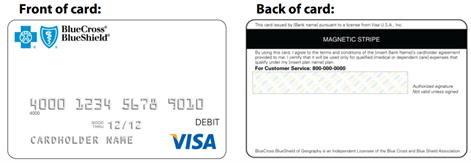

Health Care Debit Cards

Members who have CDHC plans often have health care debit cards that allow them to pay for out-of-pocket costs using funds from their Health Reimbursement Account (HRA), Health Savings Account (HSA), or Flexible Spending Account (FSA). All three are types of tax-favored accounts offered by the member’s employer to pay for eligible expenses not covered by the health plan.

Some cards are “stand-alone” debit cards to cover out-of-pocket costs while others also serve as a Member ID card with the member’s ID number. These debit cards can help you simplify your administration process and can potentially help:

- Reduce bad debt

- Reduce paper work for billing statements

- Minimize bookkeeping and patient account functions for handling cash and checks

- Avoid unnecessary claim payment delays

In some cases, the card will display the Blue Cross and Blue Shield trademarks along with the logo from a major debit card such as MasterCard® or Visa.®

Example: Stand-alone health care debit card

Example: Combined health care debit card and Member ID card

The health care debit card includes a magnetic strip allowing providers to swipe the card to collect the member’s cost-sharing amount (i.e., copayment). With health care debit cards, members can pay for copayments and other out-of-pocket expenses by swiping the card through any debit card swipe terminal. The funds will be deducted automatically from the member’s appropriate HRA, HSA, or FSA account.

Combining a health insurance ID card with a source of payment is an added convenience to members and providers. Members can use their cards to pay outstanding balances on billing statements. They can also use their cards via phone in order to process payments. In addition, members are more likely to carry their current ID cards because of the payment capabilities.

If your office currently accepts credit card payments, there is no additional cost or equipment necessary. The cost to you is the same as the current cost you pay to swipe any other signature debit card.

Helpful Tips

The following tips will be helpful when you are presented with a health care debit card:

- Carefully determine the member’s financial responsibility before processing payment. You can access the member’s benefits and accumulated deductible by using online electronic capabilities or by contacting the BlueCard Eligibility Line at 800-676-BLUE (2583).

- You may use the debit card for member responsibility (i.e., copay) for medical services provided in your office. Please do not use the card to process full payment upfront.

- You may choose to forego using the debit card on the date of service and wait for the claims to be processed by Highmark to determine the member’s responsibility.

- All services, regardless of whether or not you have collected the member responsibility at the time of service, must be billed to Highmark for proper benefit determination and to update the member’s claim history.

Questions? If you have any questions about the member’s benefits, check eligibility and benefits electronically or by calling 800-676-BLUE (2583).

For questions about the health care debit card processing instructions or payment issues, please contact the toll-free debit card administrator’s number on the back of the card.

The Patient Protection and Affordable Care Act of 2010 provides for the establishment of Health Insurance Marketplaces (or “Exchanges”) in each state where individuals and small businesses can purchase qualified coverage. These exchanges are websites through which eligible consumers may purchase insurance.

The Marketplaces are intended to create a more organized and competitive marketplace for health insurance by offering members a choice of health insurance plans, establishing common rules regarding the offering and pricing of insurance, and providing information to help consumers better understand the options available to them. The Marketplaces will enhance competition in the health insurance market, improve choice of affordable health insurance, and give individuals and small businesses purchasing power comparable to that of large businesses.

The Marketplaces offer consumers a variety of health insurance plans. Product and Plan information, such as covered services and cost sharing (i.e., deductibles, coinsurance, copayments, and out-of-pocket limits) are organized in a manner that makes comparisons across health insurance plans easier for consumers.

In conjunction with offering a choice of health insurance plans, the Marketplace is intended to provide consumers with transparent information about health insurance plan provisions such as premium costs and covered benefits as well as a plan’s performance in encouraging wellness, managing chronic illnesses, and improving consumer satisfaction.

Marketplace Options

Each state was given the option to set up its own “state-based” Marketplace approved by the Department of Health and Human Services (HHS) for marketing products to individual consumers and small employers. If the state did not set up a state-run marketplace, HHS has established either a federally-facilitated Marketplace or a Federal partnership Marketplace in the state.

Blue Plans that offer products on the Marketplaces collaborate with the state and federal governments for eligibility, enrollment, reconciliation, and other operations to ensure that consumers can seamlessly enroll in individual and employer-sponsored health insurance products.

Pennsylvania has a Federally Facilitated Exchange (FFE) marketplace. The federal government, mainly through the Department of Health and Human Services, will operate nearly all of the functions. It will verify eligibility for buying coverage, determine subsidies, and oversee enrollment, plan management, consumer assistance, and financial management.

Delaware and West Virginia are two of the seven states that formed state-federal partnerships with the states operating the plan management and consumer assistance functions of the Marketplace.

OPM Multi-State Plan Program

Under the Affordable Care Act (ACA) of 2010, the Office of Personnel Management (OPM) was required to offer OPM-sponsored products on the Marketplaces beginning in 2014. For a coverage effective date of January 1, 2015, Blue Cross and Blue Shield Plans participated in this program by offering these Multi-State Plans on Marketplaces in 33 states and the District of Columbia, including Highmark in Pennsylvania, Delaware, and West Virginia. The ACA requires these products to be offered across all states and the District of Columbia by 2017.

These products are similar to the other Qualified Health Plan products offered on the Marketplaces. Generally, all of the same requirements that apply to other State Marketplace products also apply to these Multi-State Plan products.

Exchange Individual Grace Period

The Patient Protection and Affordable Care Act (PPACA) mandates a three-month grace period for individual members who receive a premium subsidy from the government and are delinquent in paying their portion of premiums. The grace period applies as long as the individual has previously paid at least one month’s premium within the benefit year. The health insurance plan is only obligated to pay claims for services rendered during the first month of the grace period. PPACA clarifies that the health insurance plan may pend claims during the second and third months of the grace period.

Blue Plans are required to either pay or pend claims for services rendered during the second and third month of the grace period. Consequently, if a member is within the last two months of the federally-mandated individual grace period, providers may receive a notification from Highmark indicating that the member is in the grace period.

Claims and Utilization Review

Providers should follow current practices with Highmark for claims processing and handling of Marketplace claims. You can make claim status inquiries through Highmark or by submitting an electronic inquiry to Highmark.

If authorization/precertification is needed, you should follow the same protocol as you do for any other BlueCard members.

Blue Exchange was developed by the Blue Cross Blue Shield Association as a gateway for routing inquiries about out-of-area members between providers and the member’s Blue Plan. Blue Exchange transactions submitted through Highmark are routed to the member’s Blue Plan based on the prefix.

Blue Exchange simplifies your exchanges for out-of-area members using HIPAA- compliant transactions. There are three primary types of transactions that can be routed via BlueExchange:

- Eligibility and Benefits Inquiry and Response;

- Claim Status Inquiry and Response; and

- Referral/Authorization Requests.

Accessing Blue Exchange Via Availity

Highmark provides you with convenient, easy-to-use access to Blue Exchange via Availity. Each of these transactions can be initiated through Availity’s authorization workflow.

Electronic Transactions Routed Via Blue Exchange

If your office has the capability, the following transactions can be submitted to Highmark for out-of-area members via your practice management software and routed via Blue Exchange:

- 270 for Eligibility and Benefits

- 276 for Claim Status

- 278 for Utilization Review

Highmark will route both the inquiry and response transactions between you and the member’s Blue Plan via Blue Exchange.

As a Highmark participating provider, you have three options for verifying eligibility for members of other Blue Plans:

- Submit an electronic HIPAA 270 transaction to Highmark;

- Initiate a Secure Message via Availity; or

- Call the BlueCard Eligibility line at 800-676-BLUE (2583).

Electronic Transactions Preferred

Electronic transactions and online communications have become integral to health care, and they are the preferred method of interaction between providers and Highmark. Today’s technology can help you simplify business operations, cut costs, and increase efficiency in your office.

Electronic options for verifying eligibility and benefits for out-of-area Blue Plan members provide a quick turnaround. You can use the following electronic options for verifying eligibility and benefits for an out-of-area member:

- Submit a HIPAA 270 Eligibility Inquiry transaction to Highmark: Highmark will route both the inquiry and the 271 response transactions between you and the member’s Blue Plan via BlueExchange; or

- Initiate a Secure Message via Availity.

BlueCard Eligibility Phone Line

For those offices that are not electronically-enabled, the Blue Cross Blue Shield Association provides a toll-free phone line for eligibility and benefit inquiries for BlueCard members. Contact BlueCard Eligibility at 800-676-BLUE (2583).

- English and Spanish speaking phone operators are available to assist you.

- Blue Plans are located throughout the country and may operate on a different time schedule than Highmark; you may be transferred to a voice response system linked to customer enrollment and benefits outside that Plan’s regular business hours.

- The BlueCard Eligibility Line is for eligibility, benefit, and precertification and referral authorization inquiries only; it should not be used for claim status. Direct all claim inquiries to Highmark.

Electronic Health ID Cards

Some Blue Cross Blue Shield Plans have implemented electronic health ID cards to facilitate a seamless coverage and eligibility verification process.

- Electronic health ID cards enable electronic transfer of core subscriber/member data from the ID card to the provider’s system.

- A Blue Plan electronic health ID card has a magnetic stripe on the back of the card, similar to what you can find on the back of a credit or debit card. The subscriber/member electronic data is embedded on the third track of the 3-track magnetic stripe.

- Core subscriber/member data elements embedded on the third track of the magnetic stripe include: subscriber/member name, subscriber/member ID, subscriber/member date of birth, and Plan ID.

- Providers will need a track 3 card reader in order for the data on track 3 of the magnetic stripe to be read (the majority of card readers in provider offices only read tracks 1 and 2 of the magnetic stripe; tracks 1 and 2 are proprietary to the financial industry).

- The Plan ID data element identifies the health plan that issued the ID card. Plan ID will help providers facilitate health transactions among various payers in the marketplace.

- An example of an electronic ID card:

Traditionally, many Blue Plan members have been held responsible for obtaining pre-service review from their Home Plan when receiving inpatient and outpatient care in another Blue Plan’s service area. If authorization is not obtained, the member could be subject to financial penalties.

Pre-service review is defined as the process of obtaining authorization for medical treatment prior to select procedures and services. The process is commonly referred to as precertification, preauthorization, notification, and/or pre-admission.

Inpatient Services

Effective July 1, 2014, under a Blue Cross Blue Shield Association (BCBSA) initiative, all Blue Plans must require participating providers to obtain pre-service review for inpatient facility services for out-of-area members. In addition, members are held harmless when pre-service review is required and not obtained by the provider for inpatient facility services (unless an account receives an approved exception).

These requirements apply to all fully-insured health benefit plans. However, if a self-funded employer group wishes to keep member precertification penalties in place, a formal exception can be filed with the BCBSA. If an account receives an approved exception, a member penalty could apply if pre-service review is not obtained for inpatient services.

Highmark provider contracts require participating providers to obtain pre-service review for inpatient facility services for our members and also out-of-area BlueCard® members. Highmark participating providers are also required to hold members harmless if the member’s plan requires pre-service review and the provider did not attempt to acquire an authorization.

This initiative also requires Blue Plan participating providers to keep the Home Plan informed of changes in a member’s condition. Providers must notify the member’s Home Plan within 48 hours when a change to the original pre-service review occurs, and within 72 hours for emergency and/or urgent admissions.

Note: This policy does not affect medical necessity. Services must still be medically necessary, appropriate, and a covered benefit. If, prior to service or care, the provider requests authorization and it is denied, a Highmark participating provider can bill the member if the member was informed of the denial and agreed in writing to be responsible for payment for the service or care.

Outpatient Services

Although providers are responsible for obtaining pre-service review for inpatient facility services, your out-of-area Blue Plan patients are responsible for obtaining precertification/preauthorization from their Blue Plan when required for outpatient services. However, you may contact the member’s Blue Plan for authorization on behalf of the member.

Effective November 1, 2020, Highmark is expanding our prior authorization requirements for outpatient services to include those services provided by out-of-area providers participating with their local Blue Plan. This will assure that the care our members receive while living and traveling outside of the Highmark service areas is medically necessary and managed consistently as it is throughout our service areas.

Availity portal functionality is enabled to accept authorization requests for outpatient services from out-of-area Blue Plan providers when submitted via their local portals.

Claims for services on the prior authorization list received without authorization will be denied and a request for medical records will be sent to the provider’s local Blue Plan.

Medical Policy and Precertification/Preauthorization Router for Out-of-Area Members

Highmark provides you with a tool to access Medical Policy and general precertification/preauthorization information for out-of-area members from other Blue Plans. All you need is the out-of-area member’s prefix to find the information for the home plan.

On the Provider Resource Center, select Provider Network from the main menu. You'll find the Medical Policy and Pre-Certification/Pre- Authorization Router for Out-of-Area Members under Inter-Plan Programs. This link is also available in the BlueCard Information Center.

Note: This feature is not available for members in the Federal Employee Program (FEP) or in a Medicare Advantage Program.

How to Obtain Authorization

The following options are available to you for obtaining pre-service review/pre-authorization for out-of-area BlueCard members:

- Submit an electronic HIPAA 278 transaction (Referral/Authorization) to Highmark via your practice management software. Highmark will route both the inquiry and response transactions between you and the member’s Blue Plan via BlueExchange.

- Use Availity. Select Patient Registration from the menu bar. Then choose Authorization and Referrals.

- Call BlueCard Eligibility at 800-676-BLUE (2583) and ask to be transferred to the utilization review area. Your call will be routed directly to the area that handles precertification/preauthorization at the member’s Home Plan.

When obtaining precertification/preauthorization, please provide as much information as possible to minimize potential claims issues. Providers are encouraged to follow up immediately with a member’s Blue Plan to communicate any changes in treatment or setting to ensure existing authorization is modified or a new one obtained, if needed. Failure to obtain approval for the additional days may result in claims processing delays and potential payment denials.

The member’s Blue Plan may contact you directly related to clinical information and medical records prior to treatment or for concurrent review or disease management for a specific member.

On January 1, 2014, the Blue Cross and Blue Shield Plans launched a new tool that gives providers the ability to access an out-of-area member’s Blue Plan (Home Plan) provider portal to conduct electronic pre-service review. The term pre- service review is used to refer to pre-notification, precertification, preauthorization, and prior approval, amongst other pre-claim processes.

Electronic Provider Access (EPA) enables providers to use their local Blue Plan provider portal to gain access to an out-of-area member’s Home Plan provider portal through a secure routing mechanism. Once in the Home Plan provider portal, the out-of-area provider has the same access to electronic pre-service review capabilities as the Home Plan’s local providers.

The ability to access the Home Plan's portal for pre-service review will result in a more efficient pre-service review process, reduced administrative costs for both the provider and the Blue Plan, and improved provider and member satisfaction.

Determine if Precertification is Required

You can first check whether precertification is required by the member’s Home Plan by either:

- Going to Eligibilty and Benefits Inquiry in Availity; or

- Accessing the Home Plan’s precertification requirements pages by using the Medical Policy Router available on the Provider Resource Center. (Select Provider Network from the main menu, and then select the Medical Policy and Pre-certification/Pre-authorization Information for Out-of-Area Members link.)

The seven steps below illustrate how claims flow through BlueCard:

- Member of another Blue Plan receives services from the provider.

- Provider submits claim to the local Blue Plan where the services were rendered (excluding ancillary and air ambulance services).

- Local Blue Plan recognizes BlueCard member and transmits standard claim to the member’s Blue Plan.

- Member’s Blue Plan adjudicates claim according to the member’s benefit plan.

- Member’s Blue Plan issues an Explanation of Benefits (EOB) to the member.

- Member’s Blue Plan transmits claim payment disposition to the local Blue Plan.

- Local Blue Plan pays the provider.

You should always submit out-of-area Blue Plan claims to Highmark using the applicable NAIC code as the payer code in the 837 Health Care Claim transaction. Highmark will work with the member’s Blue Plan to process the claim. The member’s Blue Plan will send an Explanation of Benefits (EOB) to the member.

Highmark will send you an explanation of payment or remittance advice. We will also issue the payment to you under the terms of our contract with you and based on the member’s benefits and coverage.

For More Information

See the NAIC Codes section of this unit for complete information on all Highmark NAIC payer codes.

Helpful Tips

Electronic claims submission is a valuable method of streamlining claim submission and processing, and results in faster payment. Following these helpful tips will improve your claim experience:

- Ask members for their current Member ID card and regularly obtain new photocopies of it (front and back). Having the current card enables you to submit claims with the appropriate member information (including the prefix) and avoid unnecessary claims payment delays.

- Consider electronic inquiries if you wish to inquire about precertification requirements before the service is provided or call 800-676-BLUE (2583) and ask to be connected with the utilization review area.

- Check eligibility and benefits to verify the member’s cost-sharing amount before processing payment.

- Indicate on the claim any payment you collected from the patient.

- On the 837I and the 837P electronic claim submission, use the Patient Amount Paid Segment (AMT01=F5 patient paid amount).

- On the 1500 Claim Form, report the amount paid in locator Box 29. This is the total of patient and other payer(s) prior paid, not just patient prior paid.

- On the UB-04, report this information in locator Box 54.

- Submit all Blue Plan claims to your local Highmark plan where the services were rendered. Be sure to include the member’s complete identification number when you submit the claim. This includes the 3-character prefix. Submit claims with valid prefixes only. Claims with incorrect or missing prefixes and member identification numbers cannot be processed. Any corrections to that information must be submitted on a new claim.

- Service Facility should be reported when services are rendered in a location other than the physician’s office. Service Facility fields are listed below.

- If no Service Facility is documented, the address of the Billing Provider’s office will be used to process your claim. Please do not submit your check or mailing address. Report the address of the Billing Provider office in the fields outlined below.

- One exception: If you are contracted with both your local Blue Cross Blue Shield or Blue Shield plan where your practice is located and the out-of-area (OOA) patient’s Home plan, always submit the claims to the patient’s Home plan.

- Note: Bill the appropriate addresses according to the instructions above using the following fields:

|

Electronic Claim Forms |

|---|

837I 5010 Institutional |

2000-2010AA |

Billing Provider Loops |

2310E |

Service Facility Loop |

|

837P 5010 Professional |

2000A-2010AA |

Billing Provider Loops |

2310C |

Service Facility Loop |

|

Paper Claim Forms |

|---|

UB 04 Institutional Paper Form |

Field #1 |

Facility Name and Address |

1500 Professional Paper Form |

Box 33 |

Billing Provider Information |

Box 32 |

Service Facility Location Information |

- Check claim status through Availity Essentials’ Claim Status Inquiry or by submitting an electronic HIPAA 276 transaction (Claim Status Request) to Highmark. All claim inquiries should be directed to Highmark and not the member’s Plan.

- Do not send duplicate claims. Sending another claim, or having your billing agency resubmit claims automatically, actually slows down the claims payment process and causes confusion for the member receiving multiple EOBs for the same services.

International Claims

The claim submission process for international Blue Plan members is the same as for domestic Blue Plan members. You should submit the claims directly to Highmark.

Note: See the section on How to Identify International Members in this unit for information on servicing members of the Canadian Blue Cross Plans.

Coding

Code claims as you would for Highmark claims.

Claim Status Inquiry

Highmark is your single point of contact for all claim inquiries.

- Availity’s Claim Status, used to view local claims, can also be used to find the latest status on OOA claims. To view OOA claims electronically, you must include the prefix when entering the member’s identification number.

Adjustments

Contact Highmark if an adjustment is required. We will work with the member’s Blue Plan for adjustments; however, your workflow should not be different. To initiate adjustments:

- Search for the claim in question via Claim Status within Availity and then initiate an adjustment request via the Claims Investigation Inquiry.

- Providers who are not Availity-enabled should submit adjustments electronically via the HIPAA 837 transaction if your office system is capable.

Provider Appeals

Provider appeals are handled through Highmark. We will coordinate the appeal process with the member's Blue Plan, if needed.

However, if you are appealing on behalf of the member, direct your inquiry to the member's Blue Plan. To inquire about the Plan’s process to initiate an appeal on behalf of the member, call the Customer Service phone number on the member's identification card.

If Claim Payment is Not Received

If you have not received payment for a claim, do not resubmit the claim because it will be denied as a duplicate. This also causes member confusion because of multiple Explanations of Benefits (EOBs).

Claim processing times can differ at the various Blue Plans. If you do not receive your payment or a response regarding your payment within 30 days, visit Availity, submit a HIPAA 276 (claim status request), or call Highmark’s Provider Service Center to check the status of your claim.

In some cases, a member’s Blue Plan may pend a claim because medical review or additional information is necessary. When resolution of a pended claim requires additional information from you, Highmark may either ask you for the information or give the member’s Blue Plan permission to contact you directly.

Coordination of Benefits

Coordination of benefits (COB) refers to how we ensure members receive full benefits and prevent double payment for services when a member has coverage from two or more sources. The member’s contract language explains the order for which entity has primary responsibility for payment and which entity has secondary responsibility for payment.

If you discover the member is covered by more than one health plan, and:

- Highmark or any other Blue Plan is the primary payer, submit the other carrier’s name and address with the claim to Highmark. If you do not include the COB information with the claim, the member’s Blue Plan will have to investigate the claim. This investigation could delay your payment or result in a post-payment adjustment which will increase your volume of bookkeeping.

- A non-Blue health plan is primary and Highmark or any other Blue Plan is secondary, submit the claim to Highmark only after receiving payment from the primary payer, including the explanation of payment from the primary carrier. If you do not include the COB information with the claim, the member’s Blue Plan will have to investigate the claim. This investigation could delay your payment or result in a post-payment adjustment which will increase your volume of bookkeeping.

Carefully review the payment information from all payers involved on the remittance advice before balance billing the patient for any potential liability. The information listed on the Highmark remittance advice as patient liability may be different from the actual amount the patient owes you due to a combination of two or more insurance payments.

Coordination of Benefits Questionnaire Available Online

Highmark depends on help from the member and/or provider to obtain accurate, up-to-date information about Coordination of Benefits (COB). The provider’s assistance with this process will eliminate the need to gather the information later, thereby reducing potential claim processing delays.

If you would like to assist, the Coordination of Benefits Questionnaire for BlueCard members is available to you on the Provider Resource Center's BlueCard Information Center page.

If you wish to have the questionnaire completed by the policyholder at the time of service, you can choose to fax the completed form with the policyholder’s signature to Highmark. Be sure to use a fax cover sheet that includes contact information for your practice or facility. The toll-free fax number is provided on the instruction sheet attached to the COB form. This fax number is for provider use only for submission of BlueCard COB Questionnaires. Please do not give this fax number to members.

Or, you can ask the member to complete the form and then send it to their Home Plan — the Blue Plan through which they are covered — as soon as possible after leaving your office or facility. Members should mail the form to the Blue Plan address listed on the back of their member identification card where they will also find their Home Plan’s telephone number if they have questions.

Calls From BlueCard Members

If BlueCard members contact you with questions about claims, advise them to contact their Blue Plan and refer them to their ID card for a customer service number.

The member’s Blue Plan should not contact you directly regarding claims issues. If the member’s Plan contacts you and asks you to submit the claim to them, refer them to Highmark.

For More Information

- Visit the BlueCard Information Center on the Provider Resource Center — go the main menu at the top of the page, select Provider Network, then Inter-Plan Programs.

- Call the Highmark Provider Service Center.

The Blue Cross Blue Shield Association (BCBSA) requires Blue Plans serving as the Host Plan for out-of-area Blue Plan members to perform high-dollar prepayment reviews for certain claims and communicate results of these reviews to the members’ Home Plans. The review process must be conducted prior to passing the host claim to the Home Plan.

The Home Plan is the Blue Cross and/or Blue Shield Plan where the insured is enrolled. The Host Plan is any other Blue Plan whose contracted providers are providing health care services to a Blue Plan member outside of his or her home plan's service area.

For example, Highmark serves as the Host Plan when an out-of-area Blue Plan member (e.g., has coverage through BlueCross BlueShield of Illinois) seeks services from a Highmark participating provider in our service areas.

Therefore, a host claim would be a claim that you submit to Highmark for services you provided to an out-of-area Blue Plan member. Highmark forwards the host claim to the member’s Home Plan internally through the BlueCard electronic system, and then the Home Plan adjudicates the claim, sending the information back to Highmark in order for Highmark to reimburse you.

Requirements For Providers

Highmark requires itemized bills for all high-dollar host claims that meet the criteria below. The requirements apply regardless of how claims were submitted.

Host claims that meet the following criteria require submission of itemized bills:

- Inpatient acute care;

- Allowance of $50,000 or greater;

- All lines of business, except Medicare Supplemental/Medigap and Medicaid; and

- Any pricing methodologies that are price based on charges (e.g., percentage-based).

Note: These requirements do not apply to the following claims pricing models that do not incorporate individual services or charges due to global pricing methodology:

- Per-diem

- Flat-fee case rate

- DRG (Diagnosis-Related Group) rate

Submitting Itemized Bills to Highmark

To send an itemized bill to Highmark, you can:

- Fax itemized bills to 855-329-8191/Attention: Kelly Rizor

- Email itemized bills to HighmarkHostHighDollarReview@highmark.com

If Itemized Bills Not Received

If we do not receive an itemized bill for these claims within three days after they are submitted, they will be rejected with code E1224 – “In order to process the claim, additional information is required.” As a result, payment will be delayed. If any discrepancies are found during the High Dollar Itemized Bill Audit, the claim will be amended during initial processing and only the lines that are not eligible will be denied E5027. Highmark will advise what the discrepancies are via our discrepancy sheet. The facility will not be responsible for refiling a corrected claim.

Effective July 1, 2026, the Blue Cross Blue Shield Association (BCBSA) is mandating that all Blue Plans, including Highmark, audit claims allowing $1 million or more to ensure billing accuracy.

Important: Highmark’s policy requiring itemized bills for high-dollar claims remains in effect (see the Highmark Provider Manual's 2.6 Itemized Bills Required for High-Dollar Host Claims for more information). The new BCBSA mandate is an additional requirement for $1 million claims.

How the Audit Mandate Works

Plans — both Host and Home — will be required to perform the following activities prepay:

- Host Plan Responsibilities

- Itemized bill review

- Diagnosis Related Group (DRG) review

- Claim data and financial accuracy, including:

- Pricing review

- Plan payment policy review

- Provider contract review

- Line by line review

- Never event review

- HAC (Hospital-Acquired Conditions) review

- Core clinical editing

- Advanced editing/secondary editing

- Home Plan Responsibilities

- Benefit accuracy

- Prior authorization

- Duplicate check

- Coordination of benefits

- Clinical review (including):

- Medical necessity review

- Medication review

- Level of care review

- High-Dollar payment approval/signoff process

Medical Records

When a claim is allowing $1 million or more, timely submission of all requested medical records is mandatory for a pre-payment review. Failure to provide these records in accordance with Highmark's policies and/or contractual terms will result in claim denial.

Once medical records have been received, the claim audit will resume.

Further Evaluation

The $1 million threshold will be evaluated by the BCBSA in 2028 to determine if further changes are needed.

The National Association of Insurance Commissioners (NAIC) is the U.S. standard- setting and regulatory support organization created and governed by the chief insurance regulators from the 50 states, the District of Columbia and five U.S. territories. Through the NAIC, state insurance regulators establish standards and best practices, conduct peer review, and coordinate their regulatory oversight. NAIC staff supports these efforts and represents the collective views of state regulators domestically and internationally. NAIC members, together with the central resources of the NAIC, form the national system of state-based insurance regulation in the U.S.

NAIC codes are unique identifiers assigned to individual insurance carriers. Accurate reporting of NAIC codes along with associated prefixes and suffixes to identify the appropriate payer and to control routing is critical for electronic claims submitted to Highmark EDI (Electronic Data Interchange).

Claims billed with the incorrect NAIC code will reject on your 277CA report as A3>116, “Claim submitted to the incorrect payer.” If this rejection is received, please file your claim electronically to the correct NAIC code. Please refer to the tables below for applicable NAIC codes for your service area.

Delaware

|

NAIC Code |

Provider Type |

Products |

|---|---|---|

|

00070 |

Facility provider types |

|

|

00570 |

All other provider types |

|

New York

|

NAIC Code |

Provider Type |

Products |

|---|---|---|

|

55204 |

All provider types |

|

*Providers will continue to submit claims to Empire for Empire/Anthem members who are seen in — Albany, Clinton, Columbia, Essex, Fulton, Greene, Montgomery, Rensselaer, Saratoga, Schenectady, Schoharie, Warren, and Washington counties — that comprise the 13 counties of the Highmark Blue Shield (NENY) service region.

*Providers will continue to submit claims to Excellus for Excellus members who are seen in — Clinton, Essex, Fulton, and Montgomery counties — that comprise four of the 13 counties of the Highmark Blue Shield (NENY) service region.

Pennsylvania

|

NAIC Code |

Provider Type |

Products |

|---|---|---|

|

54771W |

Western and Northeastern regions – facility type providers (UB-04/837I) |

|

|

54771C |

Central Region facility type providers (UB-04/837I) |

|

|

54771S |

Southeastern Region facility type providers (UB-04/837I) |

|

|

54771 |

All other provider types (1500/837P) |

|

|

15460 |

All provider types |

|

West Virginia

|

NAIC Code |

Provider Type |

Products |

|---|---|---|

|

54828 |

All provider types |

|

|

15459 |

All provider types |

|

A contiguous area is generally a border county in another Blue Plan’s service area one county over from the Plan’s own service area. Per Blue Cross Blue Shield Association (BCBSA) regulations, a Plan (“Licensee”) is permitted to use its Brands outside its service area when: "Contracting with health care providers in a contiguous area or contracting with certain eligible providers located outside of the Blue Plan’s service area but not in a contiguous county that are eligible affiliates of certain hospitals located one county into an adjoining service ('Eligible Affiliates') in order to serve the Licensee’s membership, regardless of where the member lives or works."

If you are a provider located in a contiguous area, your provider contract with Highmark only applies for services rendered in that contiguous area to members of the Highmark plan operating in the state that is contiguous to the provider location. If you are an Eligible Affiliate, your provider contract with Highmark only applies for services rendered to members of the Highmark plan operating in the state that is contiguous to the location of the provider with whom the Eligible Affiliate is affiliated.

The contiguous area and Eligible Affiliate contract application limitation does not apply to ancillary providers (independent labs, durable/home medical equipment and supplies, and specialty pharmacy) or in overlapping service areas, where multiple Blue Plans share the same service area.

- Highmark Blue Shield shares the service area in the 21-county Central Region of Pennsylvania with Capital BlueCross.

- Highmark Blue Shield shares the service area in the five-county Eastern Region of Pennsylvania with Independence Blue Cross.

- Highmark Blue Shield shares the service area in the 13-county Northeastern Region of New York with Anthem and in four counties with Excellus.

In the regions listed above, overlapping service area claim filing rules apply. You can reference the What Is My Service Area Guide? to identify the counties within these service areas.

Please refer to the applicable sections in this unit for claim submission guidelines for ancillary claims and for overlapping service areas.

An overlapping service area is formed when multiple Blue Plans are licensed by the Blue Cross Blue Shield Association (BCBSA) within the same service area.

Submission of claims in overlapping service areas is dependent on what Blue Plan(s) the provider contracts with in that state, the type of contract the provider has (i.e., PPO, Traditional), and the type of contract the member has with their Home Plan.

- If you contract with all local Blue Plans in your state for the same product type (i.e., PPO or Traditional), you may file an out-of-area Blue Plan member’s claim with either Blue Plan.

- If you have a PPO contract with one Blue Plan, but a Traditional contract with another Blue Plan, file the out-of-area Blue Plan member’s claim by product type. For example, if it is a PPO member, file the claim with the Plan with which you have the PPO contract.

- If you contract with one Plan and not the other, file all claims for out-of-area members with your contracted Plan.

Within the 21-county central Pennsylvania and Lehigh Valley region, the 5-county southeastern Pennsylvania region, and the 13-county Northeastern New York region, Highmark Blue Shield markets in the same region as another Blue Plan. If you treat any Highmark member in one of these regions, you must send your claim to Highmark even if you also contract with the other Blue Plan. If you treat a member of the other Blue Plan marketing in one of these regions, you must send your claim to that Blue Plan even if you do not contract with that other Blue Plan.

Note: Overlapping service area guidelines do not apply to ancillary claims.

Ancillary providers include independent clinical laboratory, durable/home medical equipment and supplies, and specialty pharmacy providers. File claims for these providers as follows:

- Independent Clinical Laboratory: To the Blue Plan whose service area the referring provider is located.

- Durable/Home Medical Equipment and Supplies: To the Blue Plan in whose state the equipment was shipped to or purchased at a retail store.

- Specialty Pharmacy: To the Blue Plan in whose state the Ordering Physician is located.

The ancillary claim filing rules apply regardless of the provider’s contracting status with the Blue Plan where the claim is filed.

Claims for air ambulance services must be filed to the BCBS Plan in whose service area the point of pickup ZIP Code is located.

Note: If you contract with more than one plan in a service area for the same product type (i.e., PPO or Traditional), you may file the claim with either Plan.

- The air ambulance claims filing rules apply regardless of the provider’s contracting status with the BCBS Plan where the claim is filed.

- Where possible, providers are encouraged to verify member eligibility and benefits by contacting the phone number on the back of the Member ID card or calling BlueCard Eligibility at 800-676-BLUE(2583).

|

Service Rendered |

How to File (Required Fields) |

Where to File |

Example |

|---|

Air Ambulance Services |

Point of Pick-up ZIP Code: Populate item 23 on CMS 1500 Health Insurance Claim Form, with the 5-digit ZIP Code of the point of pick-up.

Where Form CMS-1450 (UB-04) is used for air ambulance service not included with local hospital charges, populate Form Locators 39-41, with the 5-digit ZIP Code of the point of pick-up. The Form Locator must be populated with the approved Code and Value specified by the National Uniform Billing Committee in the UB-04 Data Specifications Manual

|

File the claim to the Plan in whose service area the point of pick-up ZIP Code is located.* *BlueCard rules for claims incurred in an overlapping service area and contiguous county apply.

|

|

Blue Plans around the country have made improvements to the medical records process to make it more efficient. They are able to send and receive medical records electronically between Blue Plans.

This method significantly reduces the time it takes to transmit supporting documentation for out-of-area claims, reduces the need to request records multiple times, and significantly reduces lost or misrouted records.

You may get requests for medical records for out-of-area members under the following circumstances:

- Preauthorization – If you receive requests for medical records from other Blue Plans prior to rendering services (as part of the preauthorization process), you will be instructed to submit the records directly to the member’s Home Plan that requested them. This is the only circumstance where you would not submit medical records to Highmark.